Anareta

- Patrick R. Reilly

- Jan 19, 2024

- 13 min read

Waiting for La Luna

Somewhere, someplace, sometime in your recent life, you bump into an old acquaintance. You are both wearing sweaters or blazers depending on the climate.

"Bro did you hear we are going to the moon"

"For research?"

"No, Bitcoin is going to a million"

"Dollars?"

"Yea"

"Why's that?"

"Well there's this guy named Michael Saylor, his company, MicroStrategy, bought billions of dollars of Bitcoin. He was already rich from the dot com era and he's all in on Bitcoin. It is growing faster than any business can so they went all in"

"Woah that's nuts! What did MicroStrategy do before Bitcoin?"

"Business intelligence bro. He knows his shit!"

"What's business intelligence?"

"They sold employee training manuals to McDonalds or something. Think they had a hand in the extortion of franchisees via ice cream machines"

"It says here on Wikipedia that they admitted to no wrongdoing relating to an accounting fraud scandal during their stock price peak and paid $10 million in fines to the SEC"

"You wanna try any of this THC soda, it's probiotic?"

"No, I'm good man"

"We're going into a supercycle soon, rates won't rise, Bitcoin is gonna go up, it's all programmed"

"Hey I think there may be this opportunity with a sealant and fuse line auto parts accessory company that recently restructured their debt. A big 4 bank backstopped the refi with an extension flexible through 2027. They are experiencing 14%-27% higher margins on their new hybrid and electric vehicle accessory lines. Meanwhile, the average car on the road is pushing over a decade. Based on current and projected reports on average credit rating, consumer spending, and credit card debt, it seems likely people will be shopping new in the next few years. Used car prices have remained high since the pandemic and have not fallen low enough for the opportunity cost of..."

Synapses fired off in the first man's head, but no connection to reality could be reestablished. The man's mind explodes into smithereens.

"Bitcoin is going to the moon!" says the prophecy proclaimed on the internet daily. In this post I'd like to examine that claim with you. I ask you what is more likely: the purchase of 1 BTC between $25,000 and $50,000 will net a you a 2,000% - 3,900% return into the millionaire investment club? Or, something more nefarious happens? Will we all be rich together, or will there be haves and have nots? The range of evolving dogma surrounding the internet money known as Bitcoin leaves the average observer concerned to the sidelines and the novitiate believer hardened by newly-concocted gospels. A key characteristic of the "space" is people adopting the narratives of popcorn headlines at the time of their investment... the lack of reflection is disconcerting. I posit that instead of going to the moon, Bitcoin is going to the toilet. A lot has changed from 2008 until now, in fact Q1 of 2023 to today demonstrated the greatest regression for Bitcoin yet. Let's dive in to the reasons for Bitcoin's downfall.

The Cult of Money: Making Bitcoin Worse for Half a Decade

If Satoshi was the prophet, then Bitcoin code maintainers must be the apostles of stupidity. Since the 2017 block wars, every change in the function of Bitcoin has been interpreted by zealots as a positive:

Fees average over $10/transaction - Bitcoin fees hit 20-month high as miner revenues match $69K BTC price

Researchers are spamming BRC-20 Ordinals of Microsoft Paint drawings to clog the mempool and slow transactions from 8TPS to 3 TPS - The surge is driven by increasing minting of Ordinals, with nearly 1.9 million inscriptions uploaded to the blockchain over the past two weeks (86% of all BTC tx's for 6 months)

Miners coordinate to increase sanctioning users of the Bitcoin network beyond OFAC guidelines, especially those involved in the spam. After realizing this would hurt mining profitability miners conceded - Ocean has introduced block template options to allow individual miners to decide which transactions will be included in the next block

Most prominent Bitcoin developer outside of Blockstream

Bitcoin has evolved to be used in any capacity except sending money from point A to point B. Bitcoin falling to $8 per transaction is too expensive to act as a currency or money. Even Bitpay, the largest digital currency payment processor, reported 115,542 Bitcoin transactions against 109,744 Litecoin transactions for the second half of 2023. By their own logic they should rebrand to "Litpay" once consumers flip usage from Bitcoin to Litecoin. The below image from the same page shows that the aforementioned scenario has already occurred. Sometimes it's hard to update more than one part of the website at a time, sometimes you realize you're living by two truths with little overlap. Jungle author, Upton Sinclair, once said "It is difficult to get a man to understand something when his salary depends on his not understanding it." The general response to this information shocks people. They tell you not to worry as Bitcoin is a store of value. Why was no one saying this prior to the lightning network failing to deliver on its proposition?

Let's just skip to Nano already. Why progress from high fee to low fee when we could already be at no fee?

The one saving grace in the development of Bitcoin's governance is that miners don't have total censorship control. Sure miners will block transactions for the banks, the federal government, state governments, law enforcement, financial regulators, and even return accidental transactions with exorbitant fees, but they are unlikely to block transactions on someone escaping death squads or raising tomato prices. Realistically, citizens of countries experiencing hard times will already have migrated to Monero. Imagine you escape the killing fields to the West and the first thing you hear is please disclose any USB's or Bitcoin on your person for VAT tax.

A Bitcoin, a Bitcoin, my kingdom for a Bitcoin!

Tuesday January 9th, 2024

Regulatory announcements since time in memoriam have been expressed through a myriad of mediums. The town crier, city hall bulletins, newspapers hot off the press, antennae radio, television in window of store, and now Twitter. What's beautiful about social media postings, is that eyeballs are always watching. Missteps are converted into memes for eternity. Color us surprised by the manner in which the SEC approached a new controversial financial technology. The blades of the rumor mill spun a full rotation:

Monday - "SEC will approve BTC Spot ETF's."

Tuesday - SEC Twitter account hacked due to lack of security measures. Post made claiming ETF will be approved. SEC retracts and said no such guarantee.

Wednesday - SEC reluctantly announces approval of all current BTC ETP's "on an accelerated basis." SEC Chairs and Commissioners publish, remove, then republish statements.

I'm not bitter about Nano gaining slow progress and recognition in the market. Patience is a virtue. I'm definitely not as petty as the head of a federal agency who tried to confuse the investing population about whether or not a financial product, sought after for a decade, is finally available. Trading of Bitcoin ETFs started after hours on Wednesday. The SEC announced at the end of the week that it was their original intention to make the announcement Thursday. Financial derivatives for Bitcoin have had a rough start.

[1] William Shakespeare, Macbeth (1605-1606)

Both Commissioner Hester Peirce and Chair Gary Gensler related the approval to prior approvals of precious metals ETPs. Approval of gold, silver, platinum, and palladium products have only ever experienced transparent and fair valuations since! They relented that although none of their concerns regarding issues of crypto market manipulation have been resolved, the SEC will nevertheless approve all applications for Bitcoin ETFs. The SEC recognized it is not their role to police junk that can be sold to the masses, their goal is to make sure that the vehicle falls within the limits of century old securities regulation. Institutions selling other financial products must be ecstatic to support this sort of energy. They love to quietly close down the failing 3x Leveraged Honoré de Balzac Holdings ETN ($DEEZ) after realizing low demand and backwardation. People just don't love french playwrights as much as they used to. But it takes two to contango. Surely, ETF providers will not have misjudged the demand for Bitcoin.

Paper Bitcoin: What do the ETFs look like?

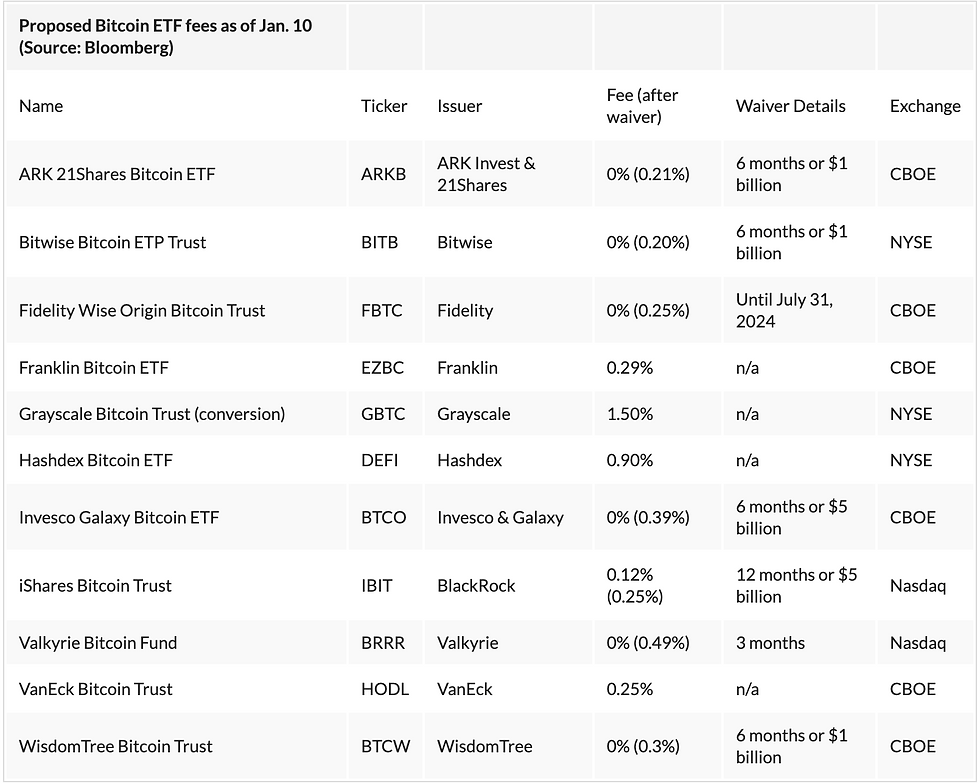

Approval of 11 Bitcoin Spot ETFs will now allow financial institutions to proffer Bitcoin exposure in a more efficient way: the institution buys & holds Bitcoin, and you buy stock in the institution. Compare the annual fee schedule in the chart below against Coinbase's 0.50%, Binance's 0.48%, Kraken's 0.20% trading fees. An aggressive allocation of 4% into Bitcoin with the average American retirement at $333,940 translates to roughly $13,000. Through a plethora of options, the intelligent investor should expect to pay $26 per year in fees at 20 bps with an ETF. Acquiring $13,000 in Bitcoin itself would include a $26 trading fee, $16.8 withdraw fee, and $8.7 network fee. Seeing how the price is roughly the same now as 3 years ago, you are paying an extra $52 to own the Bitcoin yourself, which is overall negligible.

"Bloomberg" - Investor.com

The most important caveat to investing through an ETF is that the Bitcoin you invest in will not be accessible. Most likely ever. You will own nothing and be happy. It would be significantly more efficient to process all sales of an ETF through a brokerage account and have that investor purchase Bitcoin at an exchange than to disperse the holdings through the blockchain. A hypothetical payout of Bitcoin in-kind to 1 million ETF holders would take 2 days at a rate of 7 transactions per second to fully settle. Never-mind that it would generate $8 million in fees to be shared by the fund and investor. It would also require pointless manpower verifying required information such as wallet addresses and general intent. It will be safer and easier for everyone if we use the synthetic Bitcoin instead. Good thing Bitcoin isn't backed by people accepting it as payment for products or services. What do those pesky Bitcoin developers and early adopters think they know?

The second mind-blowing aspect of the ETFs is Coinbase acting as the custodian for 9 of the 11 Bitcoin ETFs. Gemini will custody VanEck. Fidelity will self-custody (smart, smart, smart). Coinbase is a dangerous choice for a custodian because the SEC is still raging regulatory warfare against Coinbase. There is contention as to whether or not coins and tokens Coinbase offered are securities. I believe the answer lies in a case by case basis, by applying the Howey test to the governance and incentives of a network. A very minor issued when compared to a history of Coinbase employees engaging in insider trading, wash trading, and attempts to flee the country while under investigation. Coinbase also controversially declined to reveal the wallet addresses of Grayscale's Bitcoin Trusts holdings during the 2022 frenzy about proof-of-reserves (did institutions have the money they were given or was it lost, mismanaged, or stolen). Both companies continued to kick the responsibility back and forth for years. Only a week ago, former 3 Arrows Capital manager, Zhu Su, claimed that neither group can acknowledge the wallet address where the Bitcoin is stored as it would be admitting to violating SEC Rule 144 Securities Act insider/affiliate rules. Rule 144 stipulates that related parties in listed companies and those who obtain shares from related parties must comply with strict disclosure procedures when selling stocks (this type of stock belongs to restricted restricted securities or controlled securities), so as to ensure the fairness of market transactions and avoid possible insider trading information. Zhu Su would know as 3 Arrows double dipped their investment by receiving loans from Grayscale subsidiary, Genesis, and using the capital to buy newly issued shares of Grayscale's Bitcoin Trust when it traded at a premium. Coinbase will continue to act as the custodian for Grayscale; I am sure we can believe both Coinbase and Grayscale when they say they've left the tomfoolery and skullduggery behind.

Blackrock (IBIT) and Fidelity (FBTC) saw the largest activity as their funds hit the market. Bitwise (BITB) and Ark (ARKB) came in at #3 and #4 respectively. Just about everyone else should be closing up shop if they are not already. Grayscale has seen the greatest activity in their newly upgraded ETF, but mostly in the form of outflows. They claim their established trust and track record justify the extra 100 bps in fees. Elements of Grayscale's website with information related to track record and assets under management have been deleted. There won't be a clear picture of winners or losers until mid-February. Meanwhile, several platforms have blocked their investors from accessing these new products. Vanguard, Citi, Edward Jones, Merrill Lynch, Morgan Stanley and UBS have all chosen to wait before allowing their customers access to any Bitcoin ETFs. Hopefully, history will be on their side.

Planet Cracking: Miners are not Prepared for Future Prices

There is a Bitcoin halving expected to occur sometime in April or May that will cut block rewards from 6.25 to 3.125. Fears are stoked that this may eliminate poorly capitalized miners who joined during the 2019 - 2021 rally. Most miners report that they will need Bitcoin to maintain a price between $50,000 - $60,000 to maintain operations. Remember:

Mining Revenue = Fees + Block Subsidy Reward

When miners don't hit the magic number range, expect fees to rise. Rising fees generally dissuade usage of Bitcoin. It's a chicken or the egg outcome with no simple victory for either the user or miner.

Mining has grown far beyond its initial goal: the industry was built around the idea that anybody wanting to use Bitcoin would passively support the network with a CPU from an old computer. Satoshi did not anticipate GPU's or massive ASIC farms negotiating with electric companies on fixed energy pricing inputs. I doubt that Satoshi would expect 25% of Bitcoin's hashrate to turn off due to colder than expected weather in the United States. Sorry cypherpunks, the farmers almanac was incorrect this time, please come back in April to use your magic internet money.

U.S.-based Foundry is the largest Bitcoin mining pool. Foundry is also part of a small family of sister companies: the lovely bankrupt lending platform, Genesis (owes Gemini/Winklevii $600m), the tauntingly unintelligible propaganda publisher, CoinDesk, and the unabashedly inefficient Grayscale Bitcoin Trust, which recently gained approval to become an ETF. Papa Barry Silbert of parent company Digital Currency Group (DCG) recently announced that he will be stepping down. Rumors are circulating it may be due in part to an alleged overdose of civil suits brought against him and DCG by US regulators, competitors, partners, and customers.

Miners should also fear the unraveling of the biggest buoy to the price of Bitcoin: Tether. Tether (USDT), the most liquid and correlated digital currency to Bitcoin, recently put on a bizarre public relations show with their vendor, Cantor Fitzgerald, claiming to be fully backed on their $86 billion deposits. A few days after this interview and approval of the Bitcoin ETFs, Tether's reserves grew by $12 billion, almost touching $100 billion in market capitalization. This is 12x as much capital inflow than the cheaper and more efficient Bitcoin ETFs. Why? Our best guess is that through some unholy fractional-reserve lending-pact between Tether and various exchanges, there is a struggle to keep the price afloat while the ETFs are creating positions around Bitcoin. A fella I know, who helped expose Tether in 2017 for not backing its reserves 1 to 1, tells me they think Tether realistically holds 1%–3% of their claimed holdings. Time will tell. Tether's wikipedia page reads like the CIA sent their Z-team on a semi-important mission.

If you truly believe in Bitcoin, it was always cheaper to buy it directly from an exchange than to mine it. I am deeply confused by the people who allegedly sent a rogue bank more money than the ETF's generated in their first week. There is a looming darkness for financial models built around the fundamental idea that number-go-up. An attaché industry like crypto mining is hard-fought to survive number-go-sideways. Number-go-down will be its coup de grâce.

Who is financially secure enough to acquire someone else!?

Earthbound: I Used Bitcoin. It Didn't Work.

I can't let go of the memory of the first shareholder meeting we had in August 2022. I planned to send a $5 BTC transaction through the lightning network alongside a $5 Nano transaction. When trying to pass go, I was met with a rejection by the lightning channel for not proposing a high enough fee. The recommendation from the wallet itself of $0.05 was insufficient. I was astonished. In theory, there was enough time to send a Bitcoin transaction at the beginning of the meeting and have it arrive towards the end given confirmation times were between 37min - 55min at the time. Simultaneously the Nano transaction completed in about .4 seconds. Befuddled after the call I tried again. It was not until incrementally raising the fee by 5 cents all the way to $0.80 did it process. It would take another $1.20 to retrieve the remaining Bitcoin from wallet two into an exchange. I had spent 40% of my money on fees.

I wanted to emphasize that I added the distorted Richard III quote as a heading before the SEC Commissioner published her statement (she quoted Macbeth). There is a real sense of tragedy in the air. Out of all the people I have encountered over the past 8 years, even those with investments in crypto clearing high 8 figures to low 9s, I am the only person I know who has bought something with a digital currency. A summary of the purchases are as follows:

I purchased $100 of Bitcoin in order to deposit onto a Belizean based Sportsbook. It took two days to clear. I didn't trust what I thought at the time was a Pacific island country with my credit card info and drivers license. I am now aware Belize is in central America. I was slapshotting .500 on NHL Threeway and lost it all later picking the #1 darts player Michael van Gerwin against an unranked nobody. Unfortunately, there was a draw. There was only a measly 40,000 to 1 odds that would be the outcome.

I purchased, for $25 in Litecoin, a security and mining manual about the Litecoin network. The payment settled in 37 minutes, but I couldn't download the file for another hour. It helped solidify the desire to avoid mining and reinforce security measures. I learned a little about the merged mining with Dogecoin.

I purchased a $5 or 2.1 Nano (Ӿ) subscription to a front-end docker interface that allows easy access to governance information relating to my Nano node. I purchased a large bag of coffee beans for Ӿ20. The roaster included black tea sachets equivalent to the cost savings of avoiding traditional processing. I wrote a role-playing detective campaign and sold it to myself for Ӿ0.14 or $0.25. I made 10 microtransactions through half a dozen online games for a total of $9. Each transaction settled in less than a few seconds.

Welcome to the Dead Space: What's Next?

It is my belief that there will be at most a small pump to Bitcoin no greater than $56,000. Enough to keep the current narratives going; there is not another that can be grifted into. I think regulators are going to want to blame the next economic recession on Bitcoin, whether or not there is evidence. Any meaningful rise in interest rates may trigger an armageddon for Bitcoin: history tells us that during hard times, money flows into risk-averse assets (war bonds), not speculation (gold, Bitcoin). My biggest worry is that the end receiver of discounted Bitcoin will be retirement and pension accounts. When the investor logs into Schwab to sell their shares of the ETF, the rug will already have been pulled through Bitcoin and Tether.

We were and are still years early on the value proposition of a more efficient currency and money. The market inefficiencies, negligence, leverage, and external forces that stack up over decades to collapse into market contractions can happen overnight with digital currencies. An implosion and rebirth could be tomorrow or 5 years away. Hard telling not knowing. All I know is that all financial apps I disabled notifications for have overridden themselves to tell me to buy Bitcoin again.

It is my opinion that there is real utility and value in blockchain technology when it is accessible to every swathe of person. Bitcoin clearly does not fit that bill. It has almost become a box or shell of input and output. When we talk about a store of value, the first thing that comes to my mind is honey. It is durable, healthy, natural, consumable, non-perishable, and produced by the most important animal on the planet. But who's interested in that. Honey isn't cool, it's not sexy, it's not Bitcoin. Maybe you all go to the moon, maybe the moon comes to you.

End of Day 3, Legend of Zelda Majora's Mask, Nintendo 64, 2000

Comments